Russ Anderson is the president and CEO of Briggs Freeman Sotheby’s International Realty and the president of Pacific Sotheby's International Realty.

Russ Anderson is the president and CEO of Briggs Freeman Sotheby’s International Realty and the president of Pacific Sotheby's International Realty.

2024 was a year of steadily increasing activity in our housing markets, compared to the year prior, a trend that accelerated in the second half of the year. All year long, we observed growth in closed dollar volume for sales of single-family homes across our markets, but in the third quarter, single-family unit closings began to catch up as well, improving in some areas versus the same quarter in 2023. By the final quarter of 2024, almost every market we serve experienced increased unit sales compared to the prior year. These gains were not high enough for annual unit sales to pull ahead of the full calendar year of 2023, but the quarterly growth tells us that a shift is underway. This is the first time we have seen consistent unit growth nearly across the board in more than three years, since the pandemic sales surge finally began to slow during the second half of 2021.

At the same time, the increases in closed dollar volume we saw all year were even higher in the fourth quarter — versus last year — than last quarter.

The positive trend in our part of the country is mirroring the national picture. According to the National Association of REALTORS (NAR), existing residential unit sales of all home types rose by a seasonally adjusted annual rate of 4.8 percent in November, increasing for the second month after October posted the first uptick in a long time. Noting in December that pending sales also increased for three months, NAR chief economist Lawrence Yun says, “The worst of the downturn in home sales could be over, with increasing inventory leading to more transactions.” Yun is also forecasting a 9.3-percent year-over-year increase in existing home sales of all types and a closed sales volume increase of 11.3 percent throughout 2025, based on factors from declining mortgage rates to employment gains to improving inventory levels.

Regarding inventory, the years-long shortage has played a significant role in suppressing sales in our housing markets in recent times: If there are fewer houses to sell, unit sales will naturally decrease. But in our fourth-quarter market report one year ago, we noted that we were entering a transition period and starting to observe an uptick in new listings, alongside a relative improvement in closed dollar volume and unit sales across markets. Volume and units were not yet increasing year over year, but the declines were tracking at lower levels than previous quarters, primarily because of growing inventory.

As we predicted, rising levels in new listings became one of the prominent market trends of 2024. Economists within various organizations — from NAR to Goldman Sachs to the Mortgage Bankers Association — now agree that we should expect to see inventory becoming less restricted throughout 2025, which will allow for more closed transactions.

For now, we closed 2024 with annual growth in closed dollar volume compared to the calendar year of 2023, alongside unit sales that were either slightly down or close to flat, even as units began to climb ahead in the later months of the year. For a closer look at these metrics, market by market, explore our unique Market Moves on briggsfreeman.com. You will find valuable county, city and neighborhood sales information.

We continue to see increases in median sale prices, a trend that has remained consistent in our marketplaces for some time now. Nationally, NAR’s Yun projects a leveling from continued price growth in 2025, with prices rising at a more modest pace of 2 percent. In our markets, prices are still surging.

The increases in closed dollar volume and median sale prices are partly due to the change in product mix sold, with a higher degree of sales transacting in the higher price tiers. Price growth also reflects the competitive nature of today’s real estate market, where inventory remains constrained relative to historical norms — despite the recent uptick — leaving the balance of supply and demand still weighted in favor of sellers. We continue to encourage those homeowners considering whether to test the waters to take advantage of the strong sellers’ market and realize the greatest value for their properties.

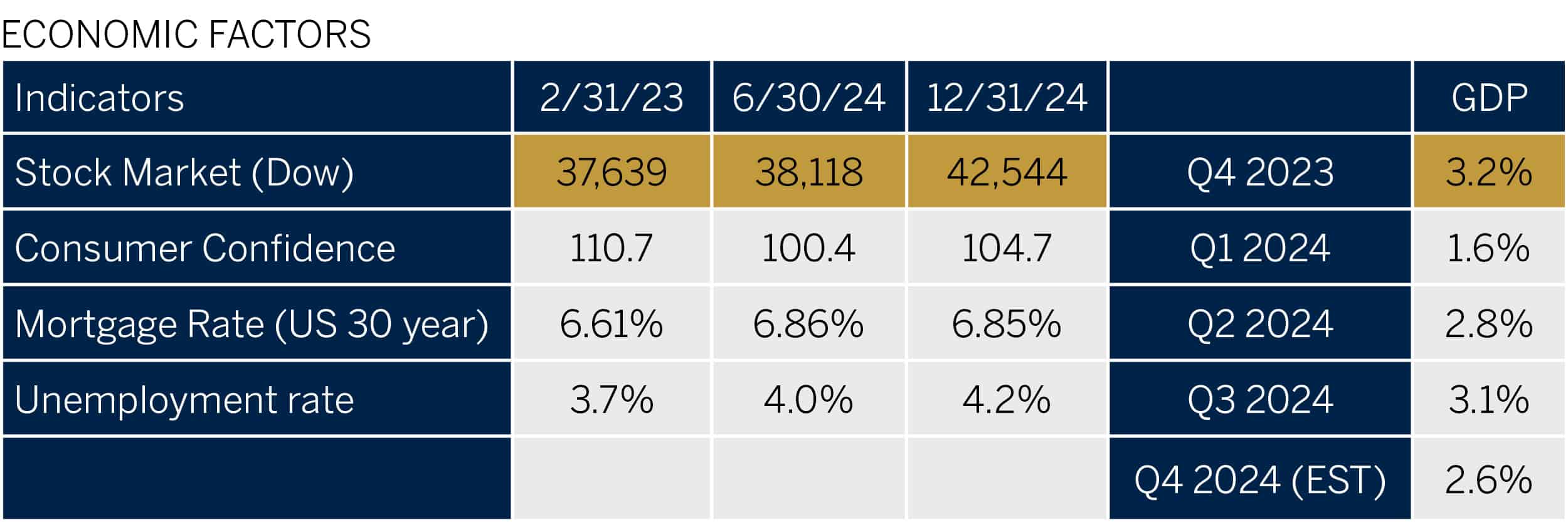

Some owners have been reluctant to enter the market, feeling hindered by the higher mortgage rates they would have to accept on a new home, which they may have purchased during a time of historically low rates of less than 4 percent. But mortgage rates have declined over the past year after peaking at nearly 8 percent in the fall of 2023. At the end of the fourth quarter of 2024, the average 30-year, fixed-rate mortgage stood at 6.85 percent, which is higher than it was at the end of the third quarter, but still represents a general trend downward. For 2025, economists from institutions such as Fannie Mae and the Mortgage Bankers Association predict mortgages to drop slightly, to 6.4 percent, while NAR paints a slightly rosier picture of 5.9 percent. As mortgages continue to inch lower, housing markets will benefit from loosening inventory and greater affordability for buyers.

Mortgages are influenced in part by the interest rates imposed by the Federal Reserve, which in turn have been influenced in part by the inflation rate. In the last quarter of 2024, for the first time since March 2020, the Fed finally cut interest rates by half a percentage point. The cut was made in response to a steady improvement in annual inflation, which has trended closer to the Fed’s target rate of 2 percent. The Fed then announced two more cuts, of a quarter-point each, the last one in mid-December. But policymakers now project only two further quarter-point cuts in 2025, fewer than previously projected, in the face of stubborn inflation data. Inflation has dropped precipitously from its mid-2022 high of 9.1 percent, but, in recent months, it has ticked up, inching from 2.4 percent for the 12 months ending in September to 2.7 percent for the 12 months ending in November. The Fed also projects a rate of inflation of around 2.5 percent next year, higher than estimated ahead of its first rate cut in September. Other economic factors showed a healthy U.S. economy as we closed out 2024, providing a strong foundation for housing markets. Unemployment remains low and relatively unchanged from Q4 2024, at 4.2 percent, holding steady in the low-4-percent range for the past several months, according to the Bureau of Labor Statistics. The U.S. Department of Commerce’s Bureau of Economic Analysis reported a healthy GDP increase of 3.1 percent for the third quarter of 2024, while the Federal Reserve Bank of Atlanta forecasts GDP growth of 2.6 percent for the fourth. Uncertainty during a presidential-election year — which historically dampens the market — is behind us.

Stock markets hit all-time highs at several points in 2024. After decreasing near the start of the last quarter, consumer confidence rose in October and November but declined again in December, to 104.7 (1985=100), according to the Conference Board’s Consumer Confidence Index.

As we look ahead to 2025, multiple positive indicators suggest a dynamic year for our real estate markets. The convergence of moderating mortgage rates, improving inventory levels and strong economic fundamentals creates opportunities for both buyers and sellers. Buyers may find more options, as inventory increases, while sellers continue to benefit from sustained demand and robust pricing. These data points, combined with our region’s enduring appeal and the return to unit sales growth we’ve observed in recent quarters, give us reason to feel bullish about our markets in 2025.

I hope you find this report informative. If we can help you with your real estate needs — or even if you want to bounce some ideas around — I invite you to contact one of our knowledgeable real estate advisors at any time. You couldn’t be in better hands.

Footer Social Links